Partner article

Think super is just for old people? Think again. It can actually be used throughout life to help you get ahead financially – including helping you save for your first home. Here are some things all young working Australians should know about the financial power that lies in their super.

1. Start early

You might glaze over at the mention of super. But if you’re in your 20s or 30s, here’s something worth staying awake for – Time and Compound Interest. Don’t yawn. Together, these two have the power to accelerate your savings growth exponentially.

Compound Interest is when you earn interest on the money you’ve saved and also on the interest that money has earned. When you combine this with Time, it means that making small regular contributions can make all the difference to your savings in the long-term.

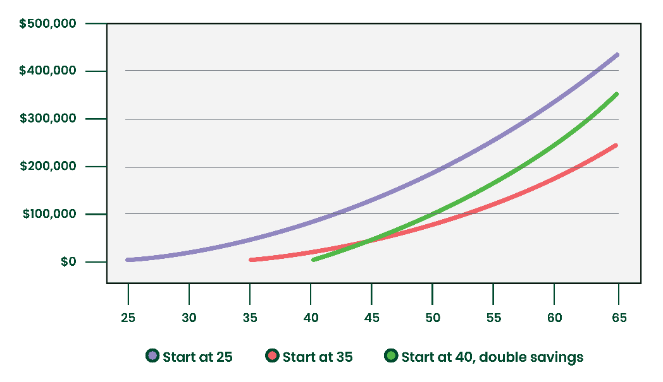

Here’s an example.

Investor A starts saving $300 a month at age 25.

Investor B starts saving $300 a month at age 35.

Investor C starts saving at age 40. To try and catch up, she commits to saving $600 each month.

Now look what happens to their savings over time. Assuming a moderate annual rate of return of 5%, you can see that Investor A who started earliest is better off.

Source: Businessinsider.com.au/compound-interest-and-young-people-2015-4

Now imagine what would happen to your super if you make some additional contributions along the way.

2. Consider chipping in a little extra

Due to the power of compound interest, any additional contributions you make to your super – no matter how small – could leave you exponentially better off over time.

For example, you could consider chipping in a little extra yourself, either by sacrificing a little bit of your salary into super or making other personal contributions.

Just remember that before-tax contributions are capped at $27,500 a year. These are called concessional contributions and they include the money your employer has to put in.

After-tax contributions are called non-concessional and these are capped at $110,000 a year. Handy to know if you get a bonus or some other windfall.

If you’re not earning very much, you might be able to get the government to chip in. Low to middle-income earners with a taxable income under $56,112 per year who make after-tax contributions to their super can apply for a top-up from the government of up to $500.

Visit the ATO website to find out more.

3.First Home Super Saver Scheme

If you’re saving for your first home, your super could help you get there sooner.

Under the First Home Super Saver Scheme, if you’re eligible, you can withdraw up to a total of $30,000 of voluntary contributions you’ve made to your super (plus earnings) to put towards a first home deposit.

Here’s how it works:

Let’s say you make additional before-tax contributions (concessional) to your super. When you’re ready to buy your first home, you can apply to withdraw a maximum of $15,000 of voluntary contributions from any one financial year, up to a total of $30,000 (plus earnings). From 1 July 2022 this will increase to $50,000.

What’s more, before-tax contributions are generally taxed at the reduced rate of 15%, while also reducing your personal taxable income. So you could enjoy tax advantages, helping you save for a house as well.

Eligibility criteria apply, so visit the ATO website to find out more.

4. Choose the right super fund

You’ll be contributing to super your whole working life, so it pays to check you’re with a good fund. What kind of returns are they delivering? Did they pass the Federal Government’s MySuper performance test last year? (13 well-known super funds failed.) How do they fare on the ATO’s YourSuper comparison tool?

Active Super is one of Australia’s top-performing super funds*, we recently reduced our admin fees for the second consecutive year and we were named a leader in responsible investment by the Responsible Investment Association Australasia in its 2021 Benchmark Report.

If you’re with us, you’ve made a great choice.

To join Active Super or find out more, visit activesuper.com.au, call 1300 547 873 or follow their socials @activesuper_au.

* As at 11 January 2020, over one year Active Super is ranked among Canstar’s top five funds for 18 to 49 year-olds with a balance up to $250,000. Over five years, we are ranked second for 18 to 49 year-olds with a balance up to $250,000. Active Super passed the first MySuper performance test for the year ended 30 June 2021. Ranked among the best performing super funds on the ATO’s YourSuper comparison tool.

Disclaimer: The information provided in this newsletter is general information and is not personal advice. It does not take into account your investment objectives, financial situation or particular needs. Accordingly, you should consider your own particular circumstances, refer to the relevant Product Disclosure Statement at activesuper.com.au and consider seeking professional personal advice before making any financial decisions.